El Salvador vs. Western Union: The Fight for Financial Freedom

For most people in developed countries, the current banking system feels fine. We have checking and savings accounts. We receive paychecks and pay off our bills. Maybe we pay a small fee when making transfers or using special credit cards. It's a normal routine that doesn't feel particularly cumbersome or as if our banks are taking advantage of us.

But for those in underdeveloped or emerging countries, it feels the opposite. El Salvador is one of the poorest countries in the western hemisphere with low per capita income and chronic inflation. Roughly 70% of its population doesn't have a bank account and works in the informal economy, which is doing things like home renovations and car repairs in exchange for cash. Most Salvadorans don't have a typical "job" where they get paychecks and are taxed by the state. They live day to day by providing those services for neighbors and friends.

And that's not enough to make ends meet. That's why they rely heavily on money sent from their families and relatives working abroad. Remittance payments have long been their major source of income. In 2020, El Salvador received nearly $6 billion in remittances, which accounted for about 23% of its GDP. That staggering number shows how dependent its economy is on those working hard in foreign countries and willing to send a portion of their money back home.

But banks aren't going to let this opportunity just slip away. Banks like Western Union and MoneyGram charge ridiculous commissions. "For instance, if García [who lives and works in Canada] wants to send $10 to his cousin in San Salvador, he will pay $3.24, or a nearly 33% commission to Western Union. Even if Garcia were to send a larger sum of money, he still faces steep fees — 12.5% for a $100 transfer." (CNBC) Imagine working day and night to send money to your family back home but your bank stealing a big slice of it every time. Not to mention, it takes a few days for the money to arrive.

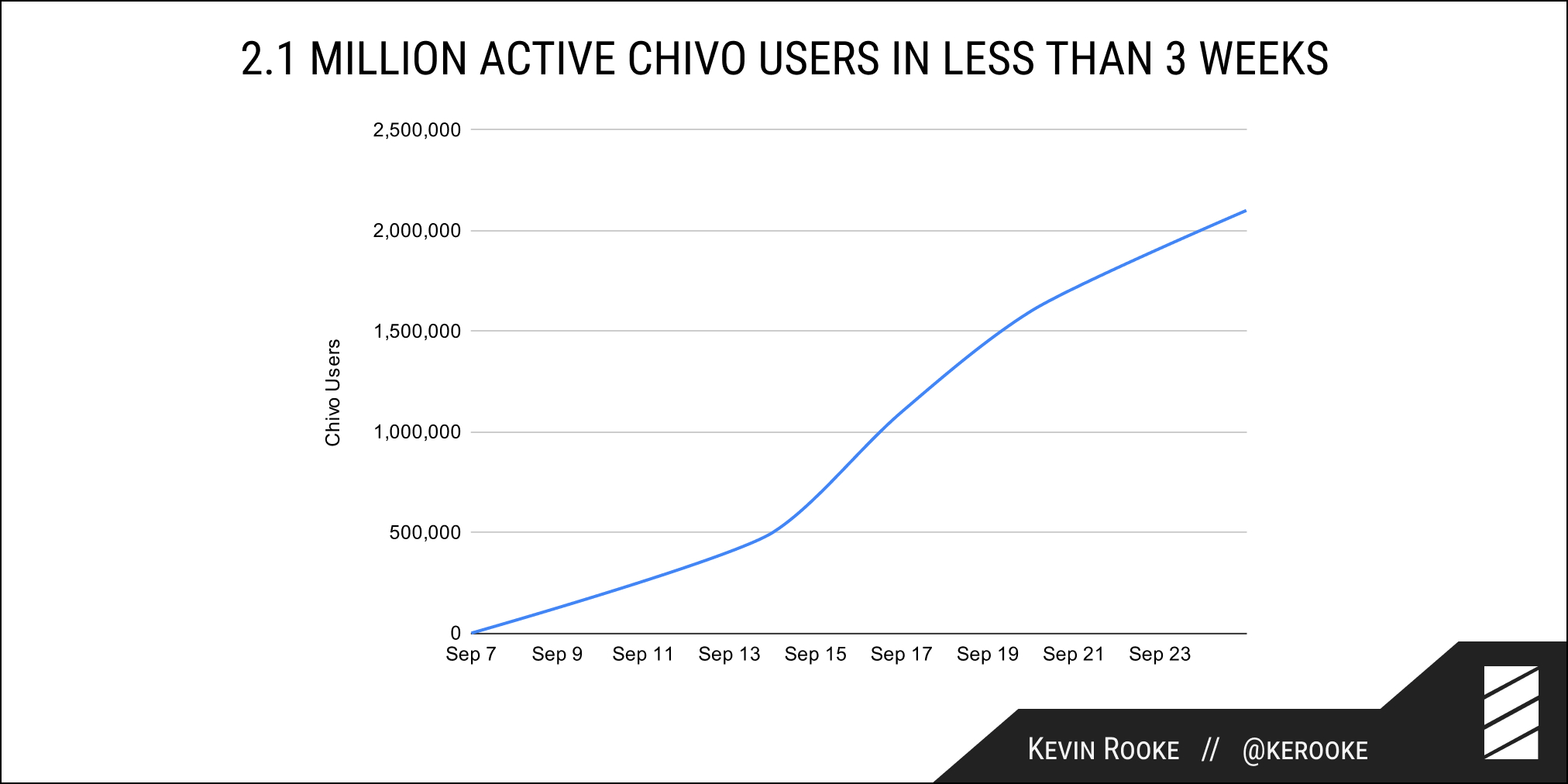

It may not be as apparent on the surface, but this is one of the many ways the traditional banking system is keeping the poor poor. And it's not like Salvadorans have many options to choose from. They have to stick to these middlemen "helping" with cross-border payments. But it's beginning to change since a few weeks ago. On September 7th, El Salvador President Nayib Bukele officially made Bitcoin their legal tender and developed a national virtual wallet called "Chivo." So far, the rate of adoption has been incredible and the benefits of using the Bitcoin’s Lightning Network are crystal clear.

If Garcia uses his self-custodial Bitcoin wallet to send the same $10 to his cousin, he'd only have to pay 10 cents, or a 1% fee. If he uses the Chivo wallet, which is reserved for Salvadorians living at home or abroad, the transaction would be free. "Once his cousin receives the funds (in a matter of minutes instead of days), he can then go to any of the 200 new Chivo ATMs the government has rolled out and withdraw U.S. dollars from his virtual wallet without a fee," said Alex Gladstein, chief strategy officer for the Human Rights Foundation. He added, "That's drop-dead stunning. It's an incredible humanitarian improvement." (CNBC)

This is how El Salvador is spearheading a major shift in the financial landscape, as the first nation to adopt Bitcoin as its official currency to bring financial inclusion to its people. President Bukele estimates that banks like Western Union and MoneyGram will lose $400 million a year because of this. That's $400 million more to Salvadorans. That's more for Garcia's family. And this is how it should be: less for the system, more for the people.

El Salvador's Bitcoin adoption is certainly controversial and an experiment we have to watch closely. There are protests against it and some are saying it's only to strengthen Bukele's dictatorship. But politics aside and from a purely financial perspective, I think it will help grow the country's economy and empower its people with more financial access and freedom. Any change takes time. But I think this change will be looked back on later as one of the most influential moments for the future of money.

🙌🏻